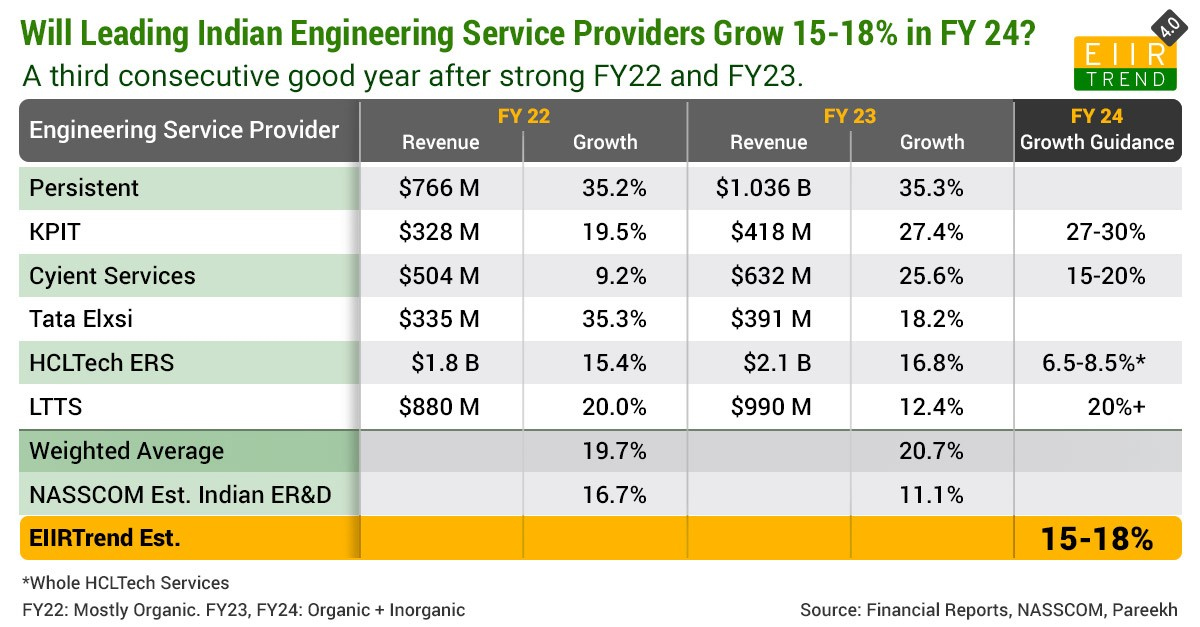

FY 23 Results of the Top Six Indian Engineering Service Providers (who declare engineering service revenue in financial results) are out. In May 2022, EIIRTrend estimated that leading Indian engineering service providers would grow 20%+ in FY23, and happy to report that we were spot on.

The weighted average YoY growth rate of these six engineering service providers in FY23 is 20.7%. The growth rate of many other large Indian engineering service providers who don’t declare their engineering revenue is in a similar range.

NASSCOM estimated the FY 23 growth rate of the Indian engineering sector as 11.1% (Strategic Review Released in February 23). The fact that leading service providers have grown more than that is an encouraging sign.

FY22 and FY23 have been two consecutive good years for engineering services. Will the engineering service growth streak continue in FY24?

Leading Indian Engineering Service Providers Growth IN 2024 H2

The Indian engineering service sector is poised for another impressive year, building on the successes of FY22 and FY23. A glance at the financial data of leading companies reveals a consistent trend of robust revenue growth, indicating a positive outlook for FY24. Let's delve into the performance of key players in this sector and explore their growth projections for the upcoming fiscal year.

Persistent Systems:

Persistent Systems witnessed remarkable growth in FY22 and FY23, with revenues reaching $766 million and $1.036 billion, respectively. The growth rates of 35.2% and 35.3% showcase the company's strong performance. As we look ahead to FY24, Persistent Systems is expected to maintain its momentum, with a continued growth projection of 15-18%.

KPIT:

KPIT experienced substantial growth in FY22 and FY23, reporting revenues of $328 million and $418 million, respectively. The growth rates of 19.5% and 27.4% highlight the company's consistent expansion. In FY24, KPIT aims to sustain its growth trajectory, estimating a robust growth range of 27-30%.

Cyient Services:

Cyient Services exhibited steady growth in FY22 and FY23, with revenues reaching $504 million and $632 million, respectively. The growth rates of 9.2% and 25.6% reflect the company's resilience and adaptability. For FY24, Cyient Services projects a growth range of 15-20%, signaling continued positive momentum.

Tata Elxsi:

Tata Elxsi demonstrated strong growth in FY22 and FY23, recording revenues of $335 million and $391 million, respectively. With growth rates of 35.3% and 18.2%, the company showcased its ability to thrive in a competitive market. Looking ahead to FY24, Tata Elxsi anticipates a growth estimation of 15-20%, underscoring its commitment to sustained success.

HCLTech ERS:

HCLTech ERS achieved significant growth in FY22 and FY23, with revenues reaching $1.8 billion and $2.1 billion, respectively. The growth rates of 15.4% and 16.8% showcase the company's steady expansion. However, for FY24, the growth projection moderates to a range of 6.5-8.5%, reflecting a more conservative outlook.

LTTS (L&T Technology Services):

LTTS reported strong growth in FY22 and FY23, with revenues of $880 million and $990 million, respectively. The growth rates of 20.0% and 12.4% demonstrate the company's resilience. For FY24, LTTS is optimistic about sustaining its growth momentum, projecting a growth rate of 20% and above.

Will FY24 be another good year for leading Indian engineering service providers despite macro uncertainties?

I think so. Some service providers have given FY23 growth guidance from the 6% to 30% range. For this cohort, we should end up with 15-18% growth on a weighted average. Four reasons for this optimism

- Big Tailwinds: Some sectors, such as automotive and aerospace, are benefiting from big tailwinds. Other engineering sectors are also doing well, and so are different geographies. Most verticals, horizontals, and geographies should deliver double-digit growth.

- Less exposure to macro headwinds: The macro headwinds in the IT sector are in BFSI and Hi-Tech verticals. Engineering service providers have relatively less exposure to these sectors. Even in hi-tech, Indian engineering service providers are holding well compared to global engineering service providers because of client and project mix.

- Large deals, orders won, and deal pipeline: There were many big deals announced in the last year by engineering service providers, which should provide stable revenue in FY24. If the trend of the large deal continues, then FY24 growth will not be difficult. The deal pipelines of service providers remain healthy.

- Inorganic pursuits: Indian engineering service providers are becoming bold and ambitious in their inorganic pursuits, be it buying another service provider or customer captive or carve-out. In FY23, many inorganic pursuits were announced, and they will help in growth in FY24. There is a possibility for further acceleration in engineering service M&As in FY24, which should be good for growth in FY24 as well.

Bottom Line: There is a lot of talk about whether the inflection point has been reached in engineering services and has pandemic become an accelerator for engineering service outsourcing the way the GFC in 2008 became an accelerator for IT outsourcing. If a cohort of leading Indian engineering service providers can grow by 20% for two consecutive years, then it will be safe to claim that the inflection point has reached for the industry and the slope of the engineering services outsourcing growth curve has changed for good. There will be short hiccups in some verticals, horizontals, and geographies in the journey, but I am an optimist of sustained engineering service growth, and FY24 should be another good year.

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Add comment