In the last quarter (Q2 CY2023), results for Indian engineering service providers were impressive. Most of them experienced double-digit growth. (Read here)

What is driving engineering services growth in this otherwise tough macro environment?

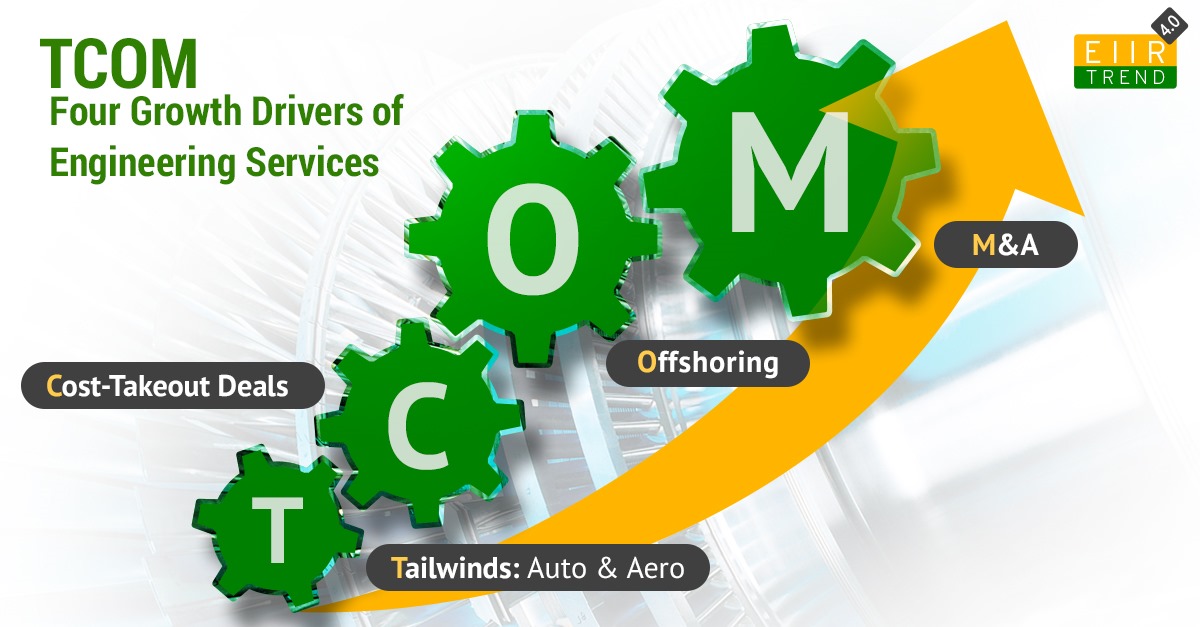

There are four major growth drivers for engineering services in this current environment: TCOM (Tailwind, Cost Take Out Deals, Offshoring, and M&A)

Tailwind: The two biggest tailwinds in engineering services are automotive and aerospace engineering

- Automotive is the biggest tailwind in engineering services. Auto enterprises are awarding large deals to engineering service providers, and the pace of large deals has increased in the last couple of years. (Read here)

- Aerospace is another significant tailwind. During the COVID pandemic, it was the most affected sector within engineering services. The decline in commercial travel adversely impacted airlines, aerospace OEMs/suppliers, and their product and engineering strategies. However, aerospace engineering has since made a robust recovery. (Read here)

Cost Take Out Deals: Enterprises are looking to reduce costs of their engineering operations. Recent examples of large cost-take out deals are across industries including Media, ISV, Hi-tech, Healthcare, BFSI, Edtech, etc. (Read here) Different deal archetypes including captive buyout, variable cost structure, vendor consolidation, product carveout, product sustenance, enterprise solution monetization, professional services carveout, etc. One good example of a large deal with many deal archetypes is Infosys – Liberty Global deal. (Read here).

Offshoring: Many enterprises are willing to offshore more engineering services to India compared to othe locations. Engineering is core work for enterprises, and there are a lot of assumptions that it can’t be outsourced, and even if outsourced, it can’t be offshored at scale. That’s the reason European service providers have a larger share because of onshore presence. But this pandemic forced enterprises to relook at these assumptions. Most work is being done virtually, so location constraint is not as big as was once believed. This is driving enterprises to rethink their engineering operating model, and there is no better place than India, which can provide engineering talent at scale and at the right price points. Offshoring has been increasing and it is evident from thatact the most global and regional engineering service providers had negative QoQ growth last quarter where as most Indian engineering service providers have positive QoQ growth.

M&A: Indian engineering service providers are becoming more assertive and ambitious in their inorganic growth strategies. They are acquiring other engineering services companies to broaden their capabilities and reach. This augmentation through acquisition focuses on three main areas: industry, services, and geography. (Read here)

More details in the NASSCOM Analyst Chat on Engineering Trends and Growth Drivers

NASSCOM Analyst Chat With Pareekh Jain On Engineering Services Results

Bottomline: There's much discussion about whether engineering services have reached an inflection point, and if the pandemic has acted as an accelerator for engineering service outsourcing, similar to how the 2008 Global Financial Crisis boosted IT outsourcing. The results from the last quarter are promising. If engineering service providers continue to harness TCOM growth drivers, we can anticipate strong double-digit growth in the upcoming quarters.

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Add comment