Private equity interest in digital engineering has come full circle from euphoria in 2021 to a reality check by 2026. What began as a period of exuberant valuations and aggressive growth is now entering a phase of more realistic assessment around scalability, differentiation, and exit viability.

Euphoria (2021): The Hitachi–GlobalLogic Moment

The inflection point came in 2021 when Hitachi acquired GlobalLogic for $9.6 billion. The deal was widely seen as a historic validation of digital engineering. An industrial conglomerate acquiring a pure-play digital engineering firm at close to 10X revenue sent a powerful signal to the market that digital engineering is a high growth, high return opportunity.

Impact (2021–2025): The PE Boom in Digital Engineering

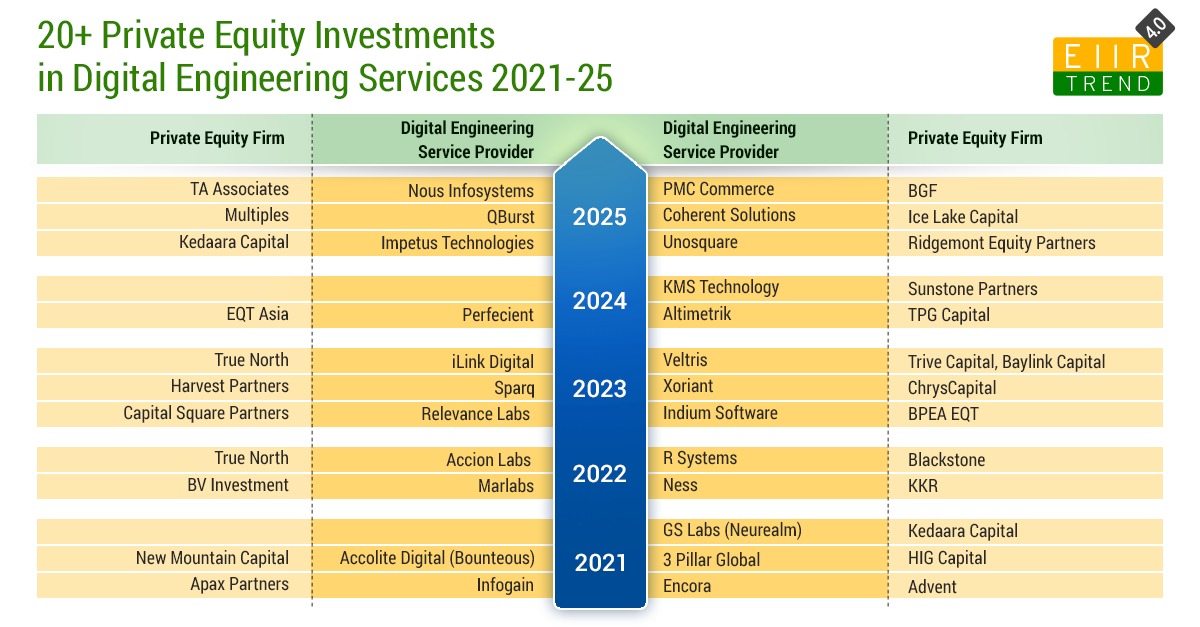

The Hitachi–GlobalLogic transaction triggered a wave of private equity activity in digital engineering services. Between 2021 and 2025, more than 20 PE-backed transactions followed, as funds rushed to replicate the perceived GlobalLogic playbook.

Some of the prominent ones are Xoriant, Ness, Neurealm, R Systems, Infogain, QBurst, Altimetrik, Perficient, and others.

In addition to post-2021 PE transactions, there are other software product engineering service providers invested by PE before 2021, such as Brillio, Apexon, Orion, following the same playbook and strategy.

Capital flowed aggressively into software product engineering, digital platforms, and enterprise engineering firms, often built through multi-acquisition roll-up strategies.

For a time, the thesis appeared sound. Digital demand surged post-COVID, enterprises accelerated platform modernization, and digital engineering firms delivered strong growth with attractive margins.

Reality Check (2026): Coforge Acquires Encora

The 2026 acquisition of Encora by Coforge for $2.35 billion marked a moment of recalibration. With FY26E revenue of approximately $600 million, the transaction valued Encora at a materially lower multiple than what investors had come to expect during the 2021 peak.

From a strategic perspective, it was a good deal for Coforge. From a private equity lens, however, it underscored the challenge of five-year value creation in digital engineering. Advent acquired Encora in 2021 for $1.5 billion and subsequently invested further through acquisitions such as Excellerate, Softelligence, and part of DMI. Exiting at $2.35 billion in 2026 delivered growth, but not the outsized returns many PE investors would have expected at entry.

What Changed: From Roaring 2021 to Crowded 2026

Several structural factors explain the shift:

- PE-on-PE competition: Post-2021, significant capital entered the same software product and digital engineering segments, often chasing similar capabilities, clients, and growth templates.

- Template saturation: The roll-up and scale model worked well in the immediate post-COVID digital demand cycle but became harder to differentiate as supply crowded the market.

- AI-led disruption: The rapid shift toward AI-led engineering has reset client expectations and delivery models, creating uncertainty around how many firms can successfully transform within typical PE holding periods.

- Longer transformation cycles: Moving from digital engineering to AI-native engineering requires deeper capability shifts than most PE time horizons comfortably allow.

What Next: Exit Options and the Need to Pivot

Exit optionality for PE firms in digital engineering is narrowing. The three primary exit routes remain:

- Sale to another private equity firm

- IPO

- Acquisition by a strategic service provider

Historically, selling to another PE fund for a “second bite at the cherry” has been the preferred route. However, for billion-dollar-plus assets in a more realistic valuation environment, this option is becoming harder to execute. While not impossible, value creation cases are now under greater scrutiny.

IPOs remain an option but are time-consuming, market-dependent, and carry execution risk.

Acquisition by another service provider is emerging as the most feasible and pragmatic exit path. These deals may involve share swaps and realistic valuation expectations rather than financial engineering-led premiums.

Preparing for a Strategic Buyer Exit

If sale to a service provider becomes the primary exit route, PE-backed firms must pivot their value-creation lens. Strategic buyers evaluate assets differently from financial investors, focusing on integration and synergy rather than standalone transformation. Key considerations include:

- Brand: The asset should enhance, not dilute, the acquirer’s brand.

- Large accounts: Presence of marquee clients that align with the buyer’s key account strategy and enable cross-selling.

- Margins: No or minimal margin dilution for the acquiring service provider.

- Geographic footprint: Strengthens existing locations and opens scalable new geographies.

- Niche capabilities: Clearly differentiated skills that help win incremental business for acquiring service providers from their existing clients.

This highlights a fundamental difference: private equity focuses on transformation potential, while service providers prioritize integration value.

Bottom Line

- Private equity enthusiasm for digital engineering is entering a reality check phase.

- The second bite at the cherry is not always as rewarding as the first.

- Exit strategies are shifting toward strategic service providers, requiring a different value-creation mindset.

- As the market matures, consolidation is inevitable and capital discipline will matter more than capital abundance.

Digital engineering remains a structurally attractive market, but the rules of the game have changed.

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Add comment