In this year-end period, rather than looking ahead and predicting trends in engineering services, I somehow chose to look back and revisit the events that defined the evolution of the industry. Over the past 12 years, I have covered engineering services as an analyst and witnessed its transformation from a niche segment to a mainstream offering and now a key growth engine of the broader IT services industry.

I have long believed that, with nearly $1.8 trillion in global R&D spending, engineering services do not face a demand problem but rather a supply challenge. Engineering service providers must continue to evolve to better support clients across their R&D journeys.

Viewed through the lens of engineering service providers, the events highlighted here have contributed meaningfully to this evolution. While each event was significant for the companies involved, their broader importance lies in how they shaped the engineering services industry by setting new directions, creating momentum, and establishing patterns for others to follow or, at the very least, to examine closely.

This note highlights 30 such events, along with their relevance. The order is loosely chronological and does not reflect their relative significance.

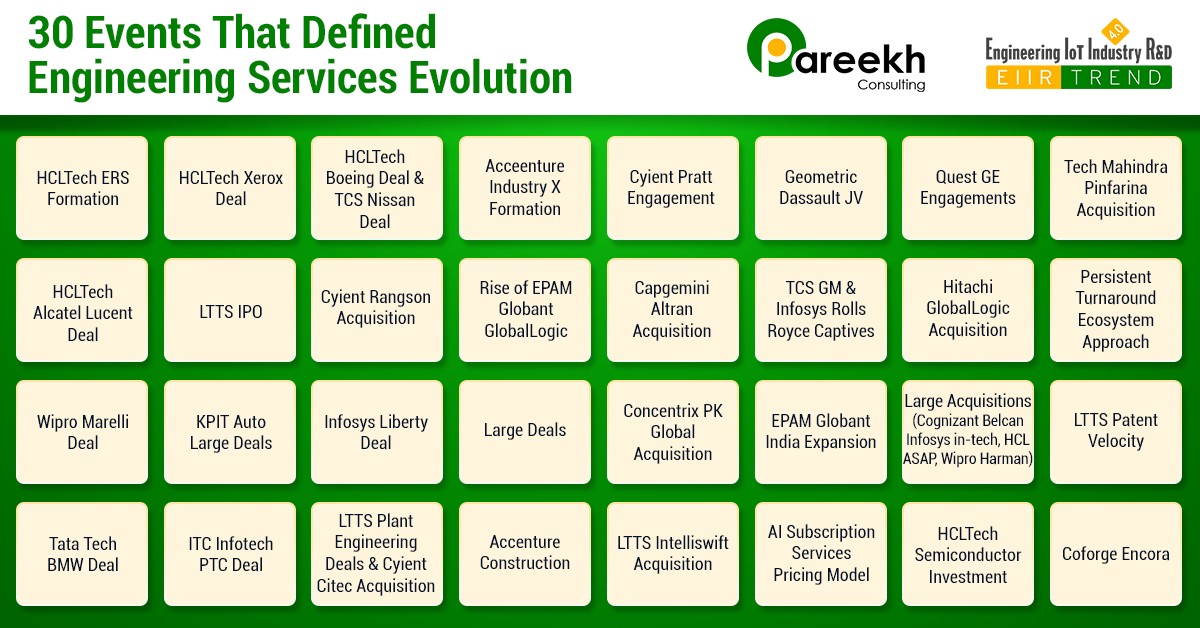

1. HCLTech ERS Formation (Strategy & Scale)

- What: While HCLTech’s R&D heritage dates back to the 1970s, the formal separation and strategic scaling of its Engineering and R&D Services (ERS) as a standalone, major horizontal distinct from traditional IT services was a pioneering move in the 2000s.

- Why it matters: This move validated engineering services as a specialized business line rather than an extension of general IT services. Prior to this, engineering capabilities were fragmented across service providers, embedded within multiple horizontals and verticals such as OPD, mechanical engineering, embedded systems, silicon, and PLM without a unified definition. HCLTech was the first to articulate engineering services holistically and subsequently became the first Indian service provider to cross $1 billion in engineering revenue, setting a blueprint for the industry.

2. HCL – Xerox Deal (2009 & Renewed)

- What: A landmark engineering partnership where HCL took over Xerox’s mechanical, electrical, and software engineering for printer product lines. The deal was renewed in 2019 for $1.3 billion.

- Why Important: This was one of the earliest large deals in engineering services and set the stage for many that followed. Structured as a total ownership model, the engagement involved a service provider managing the entire product lifecycle for a Fortune 500 OEM, demonstrating that complex product development could be successfully outsourced. It expanded the industry’s view of what was possible and encouraged service providers to pursue larger, more strategic engagements.

3. HCL – Boeing Deal / TCS – Nissan Deal

- What: HCL became a key partner for Boeing’s 787 Dreamliner (flight test computing, systems), while TCS established a deep engagement with Nissan (starting 2005) for vehicle electronics and diagnostics.

- Why Important: These deals were important for introducing unique, non-linear business models as early as the 2000s in engineering services. In these engagements, engineering service providers were compensated not for their effort, but for their output. Payments continued for years after the engagement ended, based on a share of revenue from each unit sold.

4. Geometric – Dassault Systèmes JV (2002–2016)

- What: Geometric formed a Joint Venture (3DPLM) with Dassault Systèmes, which Dassault fully acquired in 2016.

- Why Important: It pioneered the Captive–JV–Transfer model with an engineering ISV. This JV demonstrated how engineering service providers could contribute to the development of CAD software through specialized geometry expertise at scale, rather than serving merely as users of CAD tools. Following this, more engineering ISVs began to use engineering services strategically.

5. Cyient – Pratt & Whitney Engagement (2000s)

- What: A strategic partnership starting in 2000, where Cyient (formerly Infotech) became a strategic engineering partner for aero-engine components.

- Why Important: It showed the possibility of large engineering engagements in the aero engine in an outsourcing model. It opened the door for other aero engine manufacturers to leverage outsourcing with other engineering service providers.

6. Quest Global – GE Engagements

- What: Quest Global started as a partner of GE in its best days and eventually scaled this relationship across different business segments of the GE conglomerate

- Why Important: It showed the possibilities of how engineering service providers can enter and scale large engineering conglomerates as their engineering partners.

7. Tech Mahindra – Pininfarina Acquisition (2015)

- What: Tech Mahindra & Mahindra Group acquired the legendary Italian car design firm Pininfarina.

- Why Important: It was the first major design-house acquisition by an engineering service provider. The move demonstrated the potential of combining design and engineering under a single outsourcing partner. Although this trend did not gain momentum for many years, it continued to influence industry thinking. More recently, the concept has resurfaced with UST’s acquisition of an Italian design house.

8. HCLTech – Alcatel Lucent Deal (2014)

- What: A $400 million deal where HCLTech took over R&D for legacy telecom technologies from Alcatel Lucent (now Nokia), rebadging hundreds of employees.

- Why Important: This deal had several firsts. It was the first major engineering services deal executed by a sourcing advisory firm. Following this, many sourcing advisory firms attempted to establish engineering services practices. It was also the first large engineering services deal in the telecom sector, paving the way for many similar engagements across the industry. Additionally, it popularized the “carve-out” or “rebadging” model in R&D, enabling OEMs to offload mature product lines to service providers and free up capital for investment in new technologies.

9. LTTS IPO (2016)

- What: L&T Technology Services spun off from L&T and listed publicly.

- Why Important: It was the first IPO of a pure-play engineering services company of that scale in India. It brought investor focus to the ER&D sector as a distinct asset class with different growth drivers than traditional IT.

10. Cyient – Rangson Acquisition (2015)

- What: Cyient acquired Rangson Electronics, an electronics manufacturing services (EMS) company.

- Why Important: It introduced the idea of combining engineering and manufacturing. Beyond engineering services, service providers could build and prototype hardware, enabling ownership of the full value stream. Although this acquisition weighed on Cyient’s financials for several years, the business has performed well since being listed as a separate subsidiary. Nevertheless, it prompted the industry to consider the synergies between engineering and manufacturing outsourcing, a theme that is once again gaining momentum with the opening up of the EMS sector in India.

11. Accenture Industry X Formation (2017)

- What: Accenture formally launched "Industry X.0" (now Industry X), consolidating its digital engineering, manufacturing, and IoT capabilities.

- Why Important: It marked the entry of global IT giants into the ER&D space. Accenture expanded the scope of engineering services to full stack, including strategy, consulting, design, engineering, and operations, significantly increasing the total addressable market. This move triggered a broader trend of large global IT multinationals entering the engineering services domain.

12. Rise of Digital Engineering: EPAM, Globant, GlobalLogic

- What: The rapid ascent of Digital Engineering firms focused on software product engineering

- Why Important: They redefined the engineering services market by focusing on enterprise digital engineering. Prior to this shift, OPD, or software product engineering, was a niche area focused primarily on providing product engineering services to ISVs. As enterprises began building platforms rather than standalone applications, these firms positioned themselves as having stronger platform capabilities than traditional IT service providers. This marked the beginning of the digital engineering wave that most service providers eventually followed. They also demonstrated the scalability and effectiveness of the nearshore delivery model across Eastern Europe and Latin America.

13. Capgemini – Altran Acquisition (2019)

- What: Capgemini acquired Altran for €3.6 billion, creating the world's largest engineering and R&D service provider.

- Why Important: It created the industry’s first mega-player (over $5 billion) in engineering services. At the time, Altran was the world’s largest engineering service provider, and there were doubts about the scalability of engineering services as a business. This milestone marked the beginning of a new era, signaling that engineering services had truly arrived as a scalable growth engine. It also validated engineering services in the eyes of large IT players, many of whom subsequently entered the space through acquisitions.

14. TCS – GM / Infosys – Rolls Royce Captive Deals (2019/2020)

- What: TCS acquired GM’s Technical Center in India (1,300+ engineers), and Infosys took over Rolls Royce’s Bengaluru aerospace engineering center.

- Why Important: These were big captive buyouts. They demonstrated the potential for global OEMs to divest their captive centers, or GCCs, in India to service providers in order to monetize assets and gain access to broader talent pools.

15. Hitachi – GlobalLogic Acquisition (2021)

- What: Hitachi acquired GlobalLogic for $9.6 billion.

- Why Important: This was a historic validation of digital engineering. An industrial giant, Hitachi, acquired a digital engineering firm at an exceptional valuation of around 10× revenue. The transaction set the stage for a private equity boom in digital engineering services, with more than 20 PE-backed transactions following the acquisition.

16. Persistent Systems Turnaround (Ecosystem Approach)

- What: Under new leadership, Persistent pivoted to a fierce Digital Engineering focus, building a partner ecosystem with hyperscalers ( Salesforce, AWS, IBM, Google) and also PE firms.

- Why Important: It demonstrated two important points. First, mid-tier engineering service providers can win large deals while competing with much larger service providers. Second, it highlighted the power of a partner-led growth model: rather than relying solely on direct enterprise sales, engineering firms scaled by enabling the platforms of large technology companies and private equity firms.

17. Wipro – Marelli Deal (2020)

- What: Wipro secured a multi-year $270 M global automotive engineering contract with Marelli.

- Why Important: It was the largest automotive engineering services deal at that time and signalled a sustained tailwind in automotive engineering, with many large contracts subsequently awarded to engineering service providers across the industry.

18. KPIT –Demergen Auto Focus & Large Deals

- What: KPIT merged with Birlasoft and then demerged its auto business to create a focused automotive-engineering entity, winning massive deals (e.g., Renault, Honda).

- Why Important: It validated the vertical specialization thesis and rode one of the largest booms in engineering services. KPIT became one of the most significant wealth-creation journeys for shareholders and brought engineering services stocks into the attention of retail investors.

19. Concentrix – PK Global Acquisition (2021)

- What: BPO giant Concentrix acquired PK Global (formerly ProKarma) for $1.6 billion.

- Why Important: It marked the convergence of BPM and engineering. The deal demonstrated that BPM firms need strong backend engineering capabilities to design, engineer, and deliver digital journeys for their clients. This trend is accelerating in the era of agentic AI and agentic BPM, where BPM providers require significant engineering depth to drive AI-led transformation across business processes.

20. ITC Infotech – PTC Deal (2022)

- What: ITC Infotech acquired a substantial portion of PTC’s PLM implementation services business in $200M + deal.

- Why Important: This was a unique engineering professional services carve-out. A software product company, PTC, transferred its services arm to a partner to focus on pure-play software, while the partner, ITC Infotech, gained exclusive access to the product’s installed base. While professional services carve-outs are common among ISVs, this move signaled the potential of similar carve-outs for engineering ISVs as well.

21. Infosys – Liberty Global Deal (2023)

- What: A $2.5 billion deal where Infosys took over connectivity and entertainment platform engineering for Liberty Global.

- Why Important: It is the largest engineering services deal ever signed. It signalled the arrival of integrated mega deals that combine engineering, applications, infrastructure, and other domains. These integrated deal have since become major growth drivers for large IT services firms with strong engineering capabilities.

22. EPAM & Globant – India Expansion (2020s)

- What: Traditionally centered in Eastern Europe and LatAm, these firms aggressively scaled delivery centers in India.

- Why Important: It cemented India as the undisputed “global center of gravity” for engineering services, much as it had earlier for IT services. Even firms with roots elsewhere recognized that they could not scale to the next level without access to India’s depth of engineering talent. In IT services, MNCs that remain relevant today built large-scale operations in India during the 2010s. Similarly, global engineering service providers that aim to survive and thrive will need to establish scaled delivery capabilities in India.

23. Large Engineering Acquisitions By Big Indian IT Service Providers (Cognizant -Belcan, Infosys- in-tech, HCL-ASAP, Wipro-Harman)

- What: A wave of strategic engineering buys: Cognizant bought Belcan (Aero), Infosys bought in-tech (Auto), HCL bought ASAP (Auto), and Wipro acquired Harman's DTS unit.

- Why Important: These acquisitions signaled the growing importance of engineering services for large Indian IT firms. While they already had a presence in engineering, they were facing increasing competition from global MNCs and pure-play engineering service providers. The acquisitions reflected their intent to strengthen industry capabilities, expand customer access, broaden geographic footprints, and invest for the next phase of growth.

24. LTTS – Patent Velocity

- What: LTTS focused aggressively on filing patents (reaching 1000+ patents both own and with its customers)

- Why Important: It shifted the narrative that only large service providers can invest in patents, innovation, and IP. Patents enhance a firm’s innovation quotient, increase customer interest, and serve as a retention lever for high-potential talent. As a result, more pure-play engineering service providers are now actively focusing on their patent strategies.

25. Tata Technologies – BMW Deal (2024)

- What: Tata Technologies and BMW Group formed a Joint Venture (BMW TechWorks India) to develop automotive software and business IT. Its value is estimated to be $500 Million.

- Why Important: While automotive engineering outsourcing to India was booming, German automotive firms were relatively less proactive in pursuing large outsourcing engagements compared to their global peers. This large transaction signalled a shift in intent among German automakers, the positive impact of which is likely to be felt in the coming years.

26. Plant Engineering: LTTS Large Deals / Cyient – Citec Acquisition

- What: Cyient acquired Citec (Finland) to bolster plant engineering; LTTS won large deals with Exxon, bp and Shell.

- Why Important: Plant engineering has historically been a niche field in engineering services. Today, many oil and gas companies are approaching it more strategically, engaging engineering service providers, and establishing engineering GCCs in India. This shift is expected to become a significant growth driver for the industry in the coming years.

27. Accenture – Construction & Capital Projects

- What: Accenture made a series of acquisitions to enter the Construction and Capital Projects sector and made it billion dollar run rate engineering business.

- Why Important: Engineering services expanded beyond manufactured products into infrastructure, data centers, and construction, bringing digital twin and BIM technologies into the physical construction world. This highlighted the potential of construction engineering and the opportunity for engineering service providers to scale this business. In the future, more engineering service providers are likely to follow this path.

28. LTTS – Intelliswift Acquisition (2024)

- What: LTTS acquired Intelliswift for $110 million.

- Why Important: Pure-play engineering services can be broadly divided into two categories: asset-heavy sectors and software product engineering. This software-focused acquisition by one of the largest asset-heavy pure-play engineering service providers signals a convergence of these two worlds. Going forward, we can expect more asset-heavy specialists to move into software product engineering, and software-focused firms to expand into asset-heavy domains.

29. AI Pod & Subscription Services Pricing Model

- What: Firms such as Globant, EPAM, and Grid Dynamics were early adopters of the pod pricing model and have now begun piloting AI-based pod subscription and output-based pricing models.

- Why Important: If service providers are to create value from AI-led engineering and turn it into a margin lever, pricing models must evolve beyond traditional T&M and fixed-price structures toward pod-based, subscription, and output-based models. While these are still early days, this trend is expected to accelerate in the coming years.

30. HCLTech – Semiconductor Lab Investments

- What: HCL Group invested in a joint venture with Foxconn for OSAT (assembly and test), while HCLTech ERS invested in laboratories for physical testing and validation of chip prototypes prior to mass production. Many other IT Groups are investing in semiconductor subsidiaries - Tata, L&T, Cyient, etc.

- Why Important: Service providers are now investing in the physical testing of chips, not just design. As the semiconductor industry grows and India becomes an increasingly important semiconductor location, more service providers will invest across the complete value chain beyond design in India to capture a larger share of the opportunity.

31. Coforge-Encora Acquisition

- What: Coforge acquired Encora ($2.35B, Dec 2025).

- Why Important: While large IT service providers were entering engineering services through acquisitions, mid-tier IT service providers were not yet approaching the space strategically. This signalled that IT mid-tiers could also enter engineering services in a meaningful way for growth, potentially through acquisitions.

This list is by no means exhaustive, and I am certain that I have missed several important engineering services developments across different service providers.

As beauty lies in the eye of the beholder, so does the perceived importance of events in the eye of the observer. A different observer might include or exclude certain developments from this list depending on their vantage point.

The intent is to look back and celebrate how far we have come as an engineering services community. While dots are often connected in hindsight, these are some of the dots that collectively shaped the evolution of engineering services.

The journey continues. Here’s to another 30 defining moments in the years ahead. Onward and upward.

Note: I initially identified 30 events; however, during the writing process, the Coforge–Encora acquisition was announced. I considered this an important milestone to include, bringing the total to 31. This, too, signals that the engineering services market will continue to evolve likely at an even faster pace.

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Pareekh Jain

Founder of Pareekh Consulting & EIIRTrends

Add comment